Many people don’t realize that their payment history is constantly monitored and evaluated. Yet, a credit score can be the deciding factor when applying for a mortgage, car loan, or credit card. Before diving deeper, let’s clarify exactly what is a credit score and why it matters so much.

What Is Credit Score?

A credit score is a numerical value that reflects an individual’s ability to responsibly manage debt. Financial institutions rely heavily on this score to determine whether someone qualifies for a loan or credit facility.

This score is calculated based on past credit behavior, such as punctuality in paying bills, the amount of debt carried, and the types of loans previously taken. Consistently paying installments on time will improve your credit score, thereby increasing your chances of loan approval.

The Importance of Credit Scores in Loan Applications

Think of the credit score as an indirect guarantee of a person’s ability to repay borrowed money. When someone applies for a home or auto loan, financial institutions don’t have a personal relationship with the applicant. They don’t know if the person is responsible or reliable.

This is where the credit score steps in as an objective snapshot of the applicant’s financial character. A high credit score significantly boosts the likelihood of loan approval, while a low score can signal a higher risk, making lenders hesitant. Beyond approval chances, a good credit score can unlock better interest rates and higher credit limits.

The Different Levels of Credit Scores

According to Otoritas Jasa Keuangan (OJK) Regulation No. 40/POJK.03/2019, credit performance is classified into five categories, each revealing a different level of risk. Understanding these tiers helps both borrowers and lenders make smarter decisions.

1. Score 1 - Current Credit

This is the gold standard. Borrowers here pay all their dues on time, without delays. Financial institutions see them as low-risk, highly reliable, and prime candidates for new credit. If you're in this category, keep going, your financial discipline is paying off.

2. Score 2 - Special Attention

If there’s a payment delay between 1 to 90 days, the person falls into this category. While not yet considered a high risk, lenders start to view the borrower with caution.

3. Score 3 - Substandard

Missing payments for 91 to 120 days indicate serious financial trouble. At this stage, banks become more cautious and tighten approval criteria for loans.

4. Score 4 Doubtful

Payment delays between 121 and 180 days show significant doubts about repayment capability. Lenders are highly wary and often will not approve additional credit without settlement.

5. Score 5 - Bad Debt (Non-Performing Loan)

Delinquencies over 180 days classify the credit score as bad debt. Borrowers with this score face extreme difficulty obtaining new loans and may be blacklisted by financial institutions.

Benefits of Having a Good Credit Score for the Financial Industry

From the financial industry’s perspective, the credit score is an invaluable risk analysis tool. Without historical data, banks would have to manually assess each borrower, a time-consuming process with questionable accuracy.

With credit scoring systems, lenders can swiftly and precisely identify high-risk applicants, imposing stricter terms like higher interest rates or additional collateral when necessary. Conversely, applicants with high scores enjoy faster loan approvals and the possibility of more attractive interest rates.

This system also helps maintain overall financial industry stability by allowing banks to manage their credit portfolios better and minimize the risk of non-performing loans that could impact the broader economy.

How to Check Credit Score

So, how to check credit score? There are two main methods:

1. Through the Official iDebku OJK Website

Visit https://idebku.ojk.go.id, register by providing personal information, upload your ID card (KTP), and a selfie holding your ID card. After verification, usually within one working day, your credit score report will be sent via email.

2. Via Registered Financial Applications

Several third-party apps, licensed by the Financial Services Authority (OJK), allow you to check your credit score. These apps pull data from the SLIK OJK database but present it in a user-friendly format, making it easier to understand your credit standing.

Reduce Default Risk by Accurately Assessing Credit Scores

Credit scores remain the primary consideration when deciding whether to grant a loan. For financial industry players, the question is: how to effortlessly obtain and assess these credit scores?

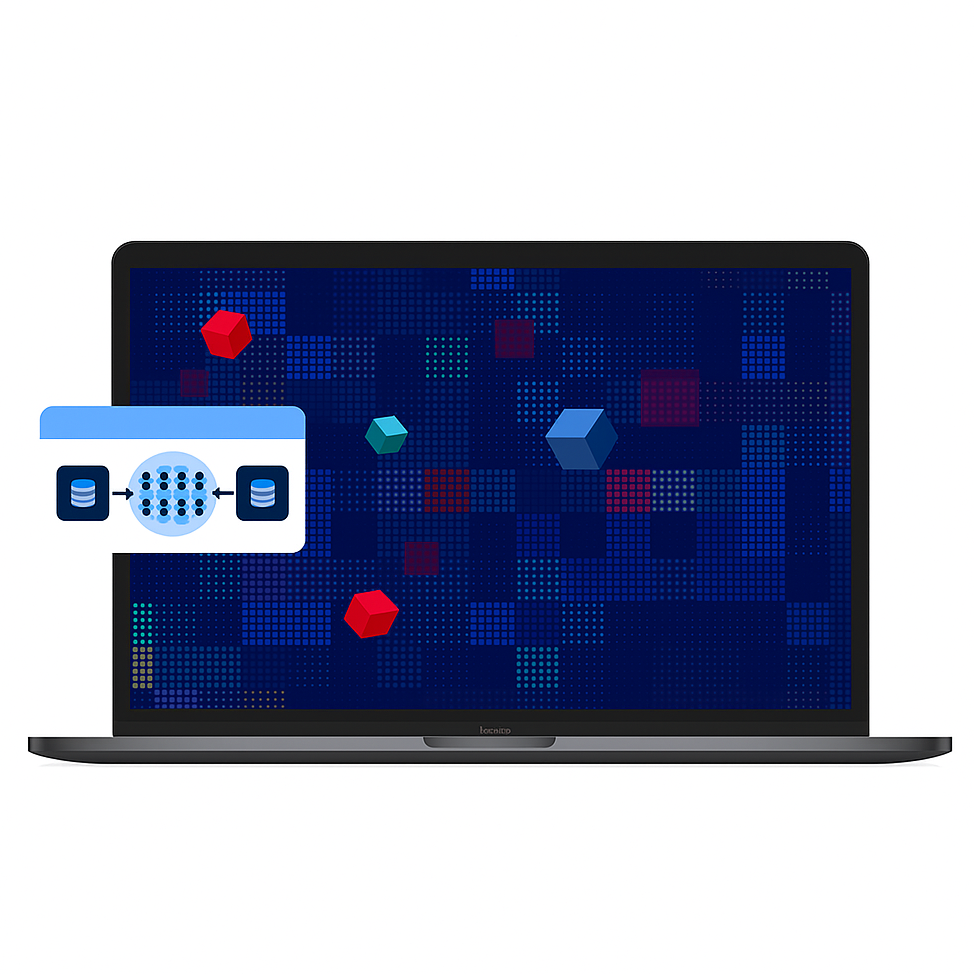

Besides using official channels like iDebku OJK or trusted financial apps, the industry must embrace innovative approaches to evaluate customer creditworthiness. Enter Telkomsel Enterprise’s Telco Insight Collaboration, a solution that enhances credit risk assessment using anonymized, encrypted digital behavior data.

Leveraging encrypted digital data via a secure Data Clean Room, this collaboration enables financial institutions to build alternative credit scores based on user behavior. This method creates a more inclusive, precise, and modern credit evaluation system that aligns with today’s digital lifestyle.

Understanding what is credit score, its main components, and how to check credit score empowers individuals and businesses alike to navigate financial decisions with confidence. Whether applying for loans or managing risk, a good credit score opens doors to better opportunities and financial stability.