Inventory isn’t just a storage space for goods, but it’s the core of operational efficiency. It ensures product availability to customers while also posing risks if mismanaged.

During global crises like the pandemic, inventory challenges became evident. As purchasing patterns changed dramatically, companies saw inventory pile up due to declining consumer demand. The overflow of unsold products not only consumed valuable warehouse space but also restricted cash flow and reduced profit margins.

This situation sheds light on a fundamental challenge in inventory management, that is fulfilling customer demand without falling into the trap of overstocking. Excess inventory doesn’t just increase storage costs, but it also ties up working capital that could otherwise be invested in growth, innovation, or operational improvements.

The situation is made even more complex by external pressures such as inflation, supply chain disruptions, and evolving consumer preferences. Optimizing your inventory, therefore, becomes more than just an operational necessity, but it’s a strategic move.

An efficient inventory strategy can help reduce holding costs, boost cash flow, and allow businesses to allocate resources more effectively. One of the most critical parts of this optimization process is choosing the right inventory management method. Two of the most widely used inventory valuation methods are FIFO (First-In, First-Out) and LIFO (Last-In, First-Out).

Each method has unique strengths and limitations, and choosing between FIFO vs LIFO depends on various factors such as your industry, pricing trends, and financial goals. This article will explore both methods in detail, including their advantages and disadvantages, to help you choose the best inventory strategy for your business.

Understanding FIFO vs LIFO

To make informed decisions about inventory strategy, it’s crucial to first understand the mechanics and implications of both FIFO and LIFO.

What Is FIFO? The First-In, First-Out Method

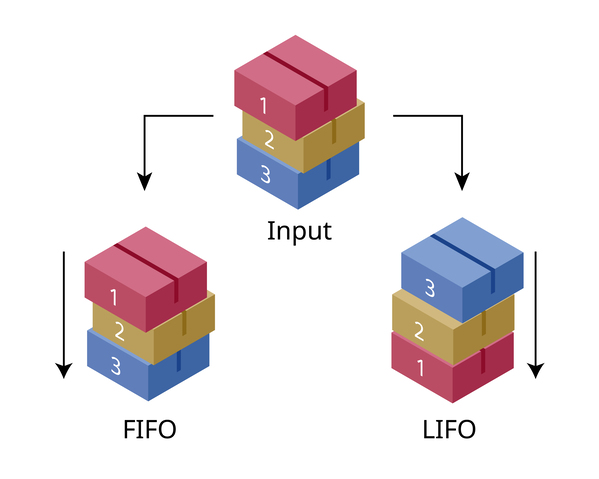

Let’s start by understanding what FIFO is. The FIFO method, short for First-In, First-Out, is an inventory valuation strategy that assumes the oldest inventory items are sold or used first. This means the goods that enter your warehouse first are the ones that get shipped out or used first.

The FIFO method is especially relevant for products that have an expiration date or degrade in quality over time, think fresh produce, dairy products, medications, or cosmetics. By using FIFO, businesses reduce the risk of spoilage, outdated stock, and customer complaints due to expired goods.

One of the major benefits of the FIFO method is that it keeps inventory flowing and ensures that older items are cleared before they lose value. It supports better stock rotation, reduces waste, and aligns with consumer expectations for freshness and quality.

From an accounting perspective, FIFO is also relatively straightforward. Since older inventory is counted as sold first, the cost of goods sold (COGS) reflects the lower cost of previous purchases. This can make a company’s financial performance look stronger in times of inflation, as the older, cheaper inventory is matched with current selling prices, leading to higher gross profits.

However, this increase in reported profit can also result in a higher tax burden. In a rising-price environment, using FIFO means the cost of goods sold is lower, so net income appears higher—and that means the company could owe more in taxes. That’s one of the main trade-offs of the FIFO method.

What Is LIFO? The Last-In, First-Out Method

Now let’s dive into what is LIFO and how the LIFO method works. LIFO stands for Last-In, First-Out. Unlike FIFO, this approach assumes that the most recently purchased or produced items are sold or used first.

The LIFO method can be particularly advantageous for companies that operate in markets where prices are steadily rising. In this scenario, the cost of goods sold will reflect the latest, often more expensive, inventory costs. As a result, the gross profit is lower, which can significantly reduce a company’s tax liability during inflationary periods.

However, the LIFO method has its own set of limitations. Since older inventory remains in storage longer, there’s a greater risk of holding outdated or obsolete products, especially items with a limited shelf life or those affected by rapid changes in technology or consumer trends. Over time, this can lead to significant losses if that unsold stock can no longer be used or sold.

Another drawback is that LIFO can undervalue your inventory on the balance sheet. Because the remaining stock is valued at older, often cheaper, prices, the total inventory value may appear lower than its current market worth. This could affect how investors or lenders perceive your business.

From an accounting standpoint, LIFO is also more complex to implement than FIFO. It requires frequent updates and adjustments to reflect the current cost of replacing inventory.

Still, in the right industry and market conditions, LIFO can offer real financial benefits, especially for managing tax liabilities strategically.

Choosing Between FIFO and LIFO: Which Strategy is Right for Your Business?

When analyzing FIFO vs LIFO, the decision goes beyond numbers, but it's about strategic alignment with your business model. Each method affects profit reporting, investor perception, and compliance differently.

Several factors play a key role in determining whether the FIFO method or the LIFO method is best for your business.

1. Type of Inventory

One of the most important considerations is the type of inventory your company handles. If your products are perishable or lose value quickly, FIFO is often the safer choice. It helps ensure that older stock is used or sold before it becomes obsolete.

On the other hand, if your inventory consists of raw materials or goods with steadily increasing prices, LIFO might be more appropriate for financial efficiency.

2. Tax Implications

Another major factor is tax implications. If you're operating in an inflationary market, LIFO can provide significant tax savings by increasing your cost of goods sold and lowering your taxable income.

However, you must also be willing to manage a more complex accounting process and accept a potentially undervalued balance sheet.

3. Financial Reporting Goals

Financial reporting goals should also influence your decision. FIFO typically results in higher net income and asset valuation, which can be attractive to investors or lenders.

Conversely, LIFO may make your company appear more conservative financially, which could be beneficial if you’re trying to minimize taxes or prepare for market uncertainty.

4. Market Conditions

Then there's the current and projected market conditions. In a stable pricing environment, FIFO might be a more transparent and easier method to maintain. But if you're expecting sustained inflation, LIFO could help you manage margins and tax obligations more strategically.

5. Strategic Visions

Finally, your long-term business strategy must be taken into account. Are you aiming for rapid growth and investor confidence, or are you more focused on financial sustainability and tax optimization?

Your inventory method should support these broader goals and align with your industry’s regulatory environment.

Conclusion

Choosing between FIFO and LIFO has its own advantages and disadvantages, which can have a significant impact on your financial statements, tax burden, and even your business’s day-to-day operations.

By considering factors such as inventory type, tax implications, financial reporting, and market conditions, you can make the right decision for your specific business situation. Your decision should be based on a thorough analysis of your operational needs, financial goals, and cost structure.

Beyond inventory methods, smart inventory management increasingly relies on technology. Telkomsel Enterprise offers a cutting-edge solution with IoT Smart Manufacturing, supporting businesses streamline operations, improve accuracy, and maximize warehouse efficiency.

Through features like Smart Manufacturing OEE, CMMS, and Smart Warehouse, companies can digitally monitor inventory and warehouse activities in real-time, reduce human errors and operational bottlenecks, increase the speed and accuracy of order fulfillment, and gain full visibility across all stages of warehouse management

These solutions allow businesses to move from traditional inventory handling to a fully integrated, digital ecosystem. That means fewer errors, faster decisions, and better results.

If you’re ready to take your inventory strategy to the next level, whether through FIFO, LIFO, or next-gen digital tools, Telkomsel Enterprise is ready to support your inventory strategy. Contact us today to learn more about how IoT Smart Manufacturing-Smart Warehouse can transform your business.